Renewable Natural Gas (RNG) is a low-carbon fuel derived from organic waste, including landfills, agricultural residues, food waste, and wastewater. Unlike fossil fuels, RNG can be blended directly into existing gas infrastructure, offering a more sustainable option to reduce greenhouse gas emissions. As global attention intensifies on decarbonisation, RNG presents an important transitional solution. But as we step further into 2025, is RNG still on a growth trajectory, or is it approaching critical limitations? This article primarily examines the state of RNG in the United States, where government incentives and clean energy mandates are helping shape the market.

Market Growth: The numbers and what’s driving them

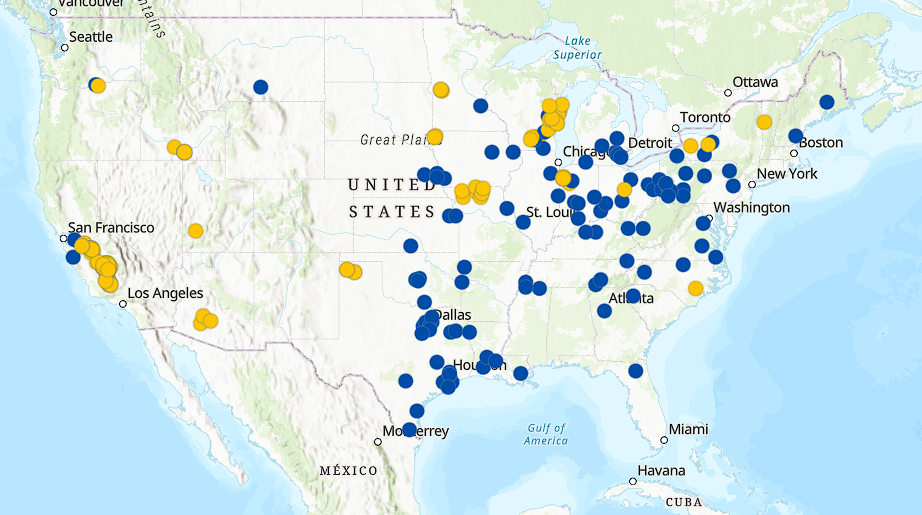

Exhibit 1: Map of Landfill and Agriculture RNG Projects in the United States

Source: Esri, USGS | Esri, TomTom, Garmin, FAO, NOAA, USGS, EPA, USFWS | United States Environmental Protection Agency

RNG remains a small but rapidly growing part of the North American energy landscape. By the end of 2025, the United States is projected to exceed 500 operational RNG facilities—a significant increase driven by both policy support and private investment. However, despite this expansion, RNG still accounts for just 0.3 percent of total natural gas production in the region. To put this in perspective, the US Energy Information Administration (EIA) expects dry natural gas production to reach 104.5 billion cubic feet per day (Bcf/d) in 2025, with RNG contributing only a fraction of that output.

The actual number of RNG projects may be higher than recorded, given that many landfills are at different stages of conversion. The US Environmental Protection Agency (EPA) maintains detailed databases which show ongoing additions across the agricultural and municipal sectors.

Policy: The engine behind RNG momentum

Policy remains the biggest driver of RNG growth. The Renewable Natural Gas Incentive Act of 2024, introduced in the US Senate, proposes a tax credit of $1 per gallon of RNG used in transportation. Such federal incentives make RNG financially viable and mitigate the cost disparity with fossil fuels.

At the state level, California continues to lead. The California Public Utilities Commission mandates utilities to procure 17.6 billion cubic feet of RNG annually by 2025, sourced exclusively from organic waste. SoCalGas, for example, aims to replace 12 percent of its conventional gas with RNG by 2030. These mandates not only ensure steady demand but also provide assurance to investors.

Other policies, such as the Renewable Fuel Standard (RFS) and the 45Z Clean Fuel Production Credit add further complexity. The 45Z credit requires physical delivery of RNG for use in transportation, which creates operational challenges, especially where gas distribution infrastructure is limited. Meanwhile, ongoing policy changes in Congress, such as through recent Ways and Means Committee proposals, are affecting investor confidence and making financial planning more difficult for developers.

Recent developments and deals: A Mixed Picture

High-profile acquisitions like BP’s $4.1 billion purchase of Archaea Energy in 2022 underscored growing investor interest in renewable natural gas (RNG). Yet, the deal was ultimately viewed by some analysts as dilutive, raising questions about valuation discipline and integration risk.

In contrast, newer developments reflect a more measured and diversified momentum increasing confidence in infrastructure-led growth across the sector. Chevron’s joint venture with Brightmark and Summit Utilities’ RNG buildout point to a shift toward operational scaling and regional expansion. TotalEnergies’ 2024 alliance with Vanguard Renewables targets the development of over 60 RNG sites across the U.S. Clean Energy Fuels and Maas Energy Works are collaborating on dairy waste-to-RNG facilities in seven states. Viridi Energy’s acquisition of a biosolids facility in Maine and Divert Inc.’s food waste conversion plants in California and Washington further illustrate the broadening feedstock base. Meanwhile, Woodland Biofuels announced plans for the world’s largest carbon-negative RNG facility in Louisiana, and Republic Services, through a joint venture with Archaea, is investing in dozens of landfill-to-RNG projects.

Together, these efforts suggest that while headline-grabbing M&A may have slowed, investor appetite is shifting toward scalable, emissions-focused platforms; indicating cautious but accelerating growth across the RNG landscape

Key challenges holding RNG back

Despite policy support and increasing investment, the RNG sector faces structural and operational constraints:

- Limited infrastructure: Many RNG producers lack access to intrastate pipeline networks. Regulatory permitting delays and restrictions introduced by previous administrations have further stalled new pipeline developments.

- High upfront capital requirements: RNG projects are expensive to build, with hidden costs including land leases, gas rights, interconnection fees, and permitting. Costs can increase further in states with more rigid regulatory oversight.

- Limited dispensing market: For RNG to qualify for credits like 45Z, it must be used in transport. However, there is a shortage of compressed natural gas (CNG) stations and vehicles, reducing potential offtake.

- Administrative complexity: Generating and tracking credits such as RINs, LCFS, or 45Z requires significant administrative effort. The lack of experienced processing partners and verification providers (e.g., for K1/K2 certificates) adds further friction.

- Pipeline and weather risk: RNG producers are sometimes unable to inject gas during adverse weather, leading to forced flaring and financial losses.

- Stakeholder expectations: Local governments and partners often demand ambitious timelines and community engagement, adding pressure to already complex projects.

Strategic role of RNG despite its modest share

Even as RNG is projected to remain below 2 percent of US natural gas consumption by 2030, its strategic importance is increasing. RNG provides immediate emissions reductions and integrates seamlessly into sectors that are hard to electrify, such as heavy-duty freight, industrial heating, and backup power generation.

For gas utilities and large consumers, RNG offers a low-disruption decarbonisation option. It allows for ESG goal alignment without requiring a complete overhaul of existing equipment or systems.

Integrating RNG into energy portfolios

RNG’s compatibility with existing infrastructure makes it an attractive transitional fuel. Its ability to reduce methane emissions by capturing waste gas also aligns it with broader climate goals and compliance obligations.

Organisations aiming to decarbonise are increasingly turning to RNG for ESG performance, supply chain resilience, and regulatory flexibility. By injecting RNG into standard gas pipelines, companies can maintain operational continuity while demonstrating environmental leadership.

Strategic success in RNG requires:

- Being realistic about market returns: With RIN prices unlikely to return to previous highs, developers need to innovate for efficiency and cost reduction.

- Diversifying revenue streams: Combining RINs, LCFS credits, and 45Z benefits can create financial stability.

- Forming strategic partnerships: Working with landfills, utilities, and feedstock suppliers ensures secure inputs and offtake agreements.

- Engaging in policy advocacy: Influencing clearer, more stable frameworks will be key to unlocking future investment and broader adoption.

A market worth watching

While Renewable Natural Gas is not the silver bullet for the energy transition, it is a critical piece of the puzzle. It reduces harmful emissions, supports rural economic development, and enables cleaner transport and industrial systems. Developers, policymakers, and investors must now work together to create a more stable and scalable market.

Despite the challenges, RNG has a bright future. With innovation, collaboration, and a realistic outlook, the industry can thrive, offering cleaner skies and more sustainable communities in the years ahead.