Something extraordinary is happening beneath the Texas sun. A state better known for oil rigs and cattle ranches is rapidly becoming the most contested patch of digital real estate on the planet, and the energy consequences may be unlike anything the grid has ever managed

Texas now leads the nation in data centers under construction, with 142 active projects, edging ahead of Virginia’s 141, according to April 2026 analysis by data firm Aterio. It is the second-largest data center market by existing inventory, but that gap is closing fast. A January 2026 Bloom Energy report projects Texas will hold nearly 30% of total US data center capacity by 2028; a 142% increase in market share from today.

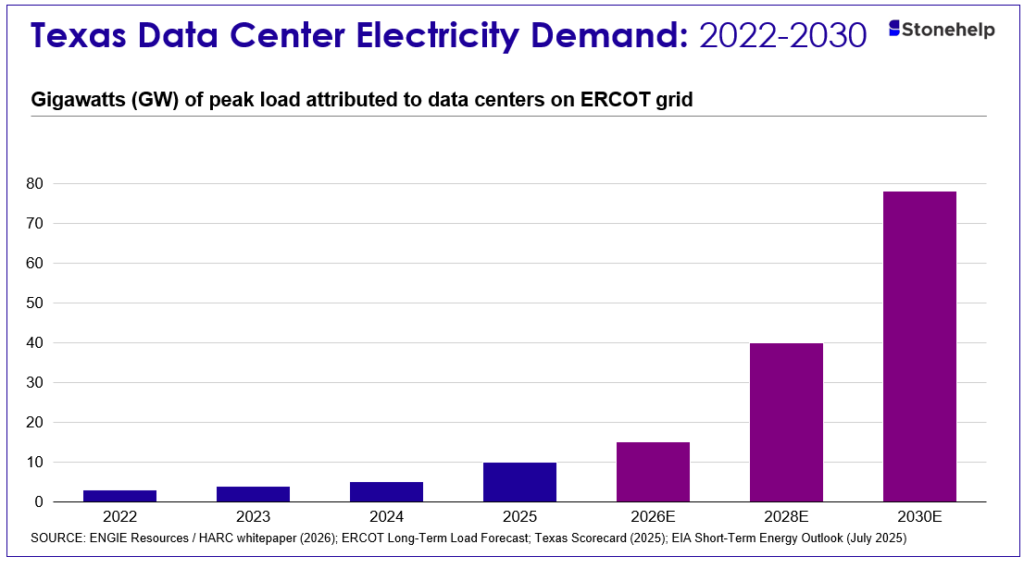

The numbers coming out of ERCOT, the state’s grid operator, are extraordinary. On April 9, 2026, ERCOT CEO Pablo Vegas stood before the Texas House State Affairs Committee and disclosed that the large-load interconnection queue had surpassed 410,000 megawatts; with 87% of it from data centers. The queue jumped by 130,000 MW in the preceding six weeks alone. That single figure, 410 GW; is nearly five times Texas’s all-time peak demand of 85,508 MW.

Not all of it will get built. Vegas himself acknowledged that. But even a fraction materializing would fundamentally reshape Texas’s energy economy.

A State of Many Centers, Not One

Unlike Northern Virginia’s single mega-cluster in Loudoun County, Texas has built a geographically distributed footprint. This dispersal is both a strategic strength and an infrastructure stress test playing out in real time.

Texas Data center growth: Six Structural Advantages

No single factor explains Texas’s rise. It is a convergence of structural advantages that, taken together, make the state the path of least resistance for hyperscale infrastructure capital.

Cheap and abundant energy. Texas commercial electricity has historically averaged 7–9 cents per kilowatt-hour. The EIA projects ERCOT demand will grow at an average rate of 11% in both 2025 and 2026; an extraordinary figure when the national average is 2.2%. Energy can represent 70% of a data center’s operating cost, so the Texas price advantage compounds dramatically at scale.

The world’s biggest wind market. Texas is the United States’ number one wind state, with over 37 GW of installed capacity, and ranks second in solar at over 16 GW installed and growing fast. For Microsoft, Google, and Meta; all committed to 100% renewable energy matching; Texas’s green power credentials are not a footnote; they are a headline. The Stargate Abilene campus is powered by a combination of West Texas wind, on-site solar, and 360 MW of on-site natural gas turbines for firm backup.

A deregulated, ‘bring your own power’ grid. ERCOT’s deregulated structure, combined with Texas policies that allow on-site generation outside traditional interconnection queues, gives data center developers unusual flexibility. Operators can install their own gas turbines or fuel cells and bypass months of utility permitting; a critical edge when AI compute timelines are measured in quarters, not years.

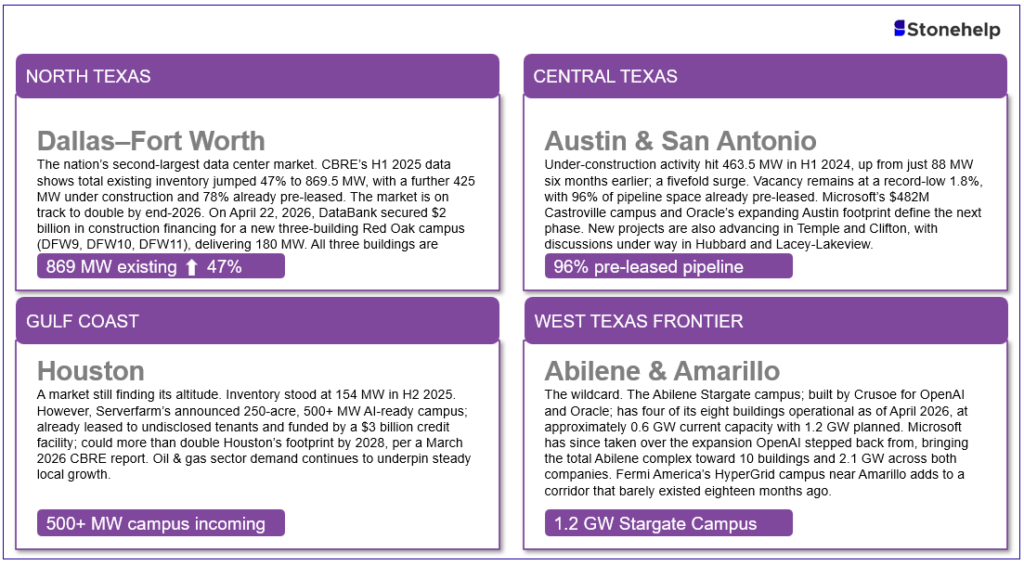

Land at scale, permitting at speed. A single hyperscale campus can require 100 to 1,000 acres. Texas has it, at a fraction of the cost of Northern Virginia or Northern California. The Abilene Stargate site alone covers roughly 1,100 acres. Rural counties with minimal zoning restrictions have welcomed projects that would face years of opposition elsewhere.

No state income tax, active incentive programs. A 2015 sales tax exemption covering electricity, hardware, and software has become a critical factor in site selection. More than 100 centers have already qualified. The Texas Comptroller’s office estimates this exemption will cost Texas $3.2 billion in foregone revenue over just the next two years; a figure the legislature is actively scrutinizing as of April 2026.

Low natural disaster risk. Absent the seismic risk of California or the hurricane belt of the Gulf Coast’s eastern flank, the Dallas–Fort Worth and Austin corridors offer geotechnical stability that matters enormously for facilities designed for 99.999% uptime.

It’s been growing rapidly over the last year and a half. And really in the last month and a half, we saw a big chunk of new projects come into this queue, jumping it up over 130,000 megawatts – Pablo Vegas, ERCOT CEO; Texas House State Affairs Committee, April 9, 2026

How Artificial Intelligence Changed Everything

Traditional enterprise data centers consumed roughly 100 to 200 watts per square foot. A modern AI training cluster can draw over 2,000 watts per square foot; a tenfold increase in power density from the same physical footprint. This is not a gradual shift; it is a step change that has made power procurement the critical path of every significant data center project.

The queue numbers from ERCOT tell the story bluntly. In December 2024, the large-load queue stood at 63 GW. By December 2025, it had nearly quadrupled to 233 GW. By April 9, 2026, it had surpassed 410 GW; adding 130 GW in just six weeks. ERCOT CEO Pablo Vegas described the speed of change as unlike anything the grid operator had previously managed, noting the existing interconnection process was designed for 40–50 large loads at a time.

ERCOT’s long-term forecast, discussed at an April 15, 2026 report to the Public Utility Commission, projects Texas electricity demand reaching over 367,000 MW by 2032; more than four times today’s record peak of 85,508 MW. The high-growth scenario, driven primarily by data centers and industrial projects, underpins the case for a fundamental rebuild of transmission infrastructure.

The Stargate initiative crystalized what AI infrastructure demand looks like at full scale. The Abilene campus, being built by Crusoe for OpenAI and Oracle, is planned at 1.2 GW across eight buildings; four of which are already operational as of April 2026. Microsoft has since picked up the adjacent expansion, with the combined Abilene complex now targeting 2.1 GW across ten buildings. That single West Texas site, on what was scrubland two years ago, will draw more power than many mid-sized cities.

Implications

1. The grid queue has outgrown the process built to manage it: ERCOT CEO Pablo Vegas told the Texas House State Affairs Committee on April 9 that the queue process was designed for 40–50 large loads at a time. It now has 410 GW in it. A new batch interconnection process is being built to replace the old system, with ERCOT hoping to present the plan to its board in June, submit to the PUC in July, and begin the first batch by August 2026. Decisions on available transmission capacity are expected in early 2027. For developers, queue position is now a strategic asset and a financing prerequisite.

2. Electricity prices will face sustained upward pressure: ERCOT’s summer 2026 peak load is projected at 90,500–98,000 MW, significantly above recent records. Adding sustained large-block AI demand tightens reserve margins and raises wholesale price frequency. CBRE noted large block leases (10+ MW) saw pricing jump up to 19% quarter-on-quarter in H2 2024. The World Economic Forum has stated it is impossible to accommodate AI data center growth and maintain grid stability without prices increasing for all customers in deregulated markets like Texas. The PUC is actively working on rules to ensure data centers; not residential customers; bear the cost of transmission upgrades their load requires.

3. Water is the constraint nobody is pricing correctly: The Texas Comptroller’s office and ERCOT are now actively surveying data centers on water usage following April 2026 legislative hearings where water scarcity emerged as a top concern. A 2026 HARC whitepaper estimates Texas data centers already consume approximately 25 billion gallons of water annually. By 2030, that could reach 2.7% of total state use in a high-growth scenario, against a backdrop where the Texas Water Development Board has already flagged a 4.8-million-acre-foot statewide supply shortfall. Several developers now use closed-loop cooling systems, with Lancium’s Abilene campus reportedly using just 20 gallons per minute against an allocation of 500; less than 5% of what was offered. But not all operators are as disciplined.

4. The tax exemption is under political pressure: Texas’s 2015 sales tax exemption for data centers; covering electricity, hardware, and software; is now one of the state’s costliest incentive programs. The Comptroller’s office projects it will cost $3.2 billion in foregone revenue over the next two fiscal years, rising to $1.8 billion annually by fiscal year 2030. The Texas House State Affairs Committee, chaired by Rep. Ken King, held hearings on April 9, 2026 and has signalled further sessions ahead of the 2027 legislative session. Industry leaders have warned that shrinking or ending the exemption would send a ‘hostile message’ to investors. The political tension is real and unresolved.

5. On-site generation is reshaping the utility relationship: Bloom Energy projects roughly one-third of all data centers will have on-site power generation by 2030. The Abilene Stargate campus has 360 MW of on-site natural gas turbines and a dedicated solar farm. ERCOT CEO Vegas noted that under the new SB 6 framework, data centers in grid emergencies must disconnect from the grid and run on their own backup generation rather than adding to scarcity conditions. This is a structural shift in how the largest power consumers relate to the grid; and it has direct implications for transmission planning, utility revenue models, and generation mix across ERCOT.

Can Texas Build Its Way Out?

Texas has done it before. In the 2010s, it built the Competitive Renewable Energy Zones transmission network; over $7 billion in new lines; to connect West Texas wind to population centers. The result was a transformation: Texas became the largest wind power market in the United States, electricity prices fell for a decade, and the state attracted the very tech investment now putting pressure on the grid it built.

The challenge today is of a different order. Between 2024 and 2025, ERCOT added approximately 23 GW of new generation capacity to the grid, with another 9 GW scheduled for early 2026. That is impressive. It is also potentially insufficient if even a significant fraction of the 410 GW queue materialises. ERCOT itself has warned the PUC not to treat high-end numbers as guaranteed outcomes, citing speculative ‘phantom’ load requests from developers holding multiple site options simultaneously.

Still, even the conservative scenarios point to a grid that must expand faster than it ever has. ERCOT’s own April 15, 2026 long-term forecast projects peak demand potentially exceeding 367,000 MW by 2032 under the high-growth scenario. The McKinsey estimate that data centers will consume 11–12% of total US power demand by 2030, up from 3–4% today, frames the national magnitude. Texas, as the country’s fastest-growing data center market, will carry a disproportionate share.

The utilities are responding. Oncor is implementing its Regional Transmission Planning Study recommendations for DFW. CenterPoint is advancing upgrades in northwest Houston. AEP Texas is managing overlapping large load and generation requests in West Texas simultaneously. A proposed 765-kV transmission backbone for the Permian Basin region is under active development, with Oncor filing its application for the Longshore Switch–Drill Hole Switch line in December 2025 and expecting regulatory approval by June 2026.

For energy professionals and infrastructure investors, the strategic question is not whether Texas will remain a data center destination. It will. The question is which participants in the energy value chain; transmission developers, gas generators, renewable project developers, battery storage operators, equipment manufacturers; will capture the value created by the largest sustained load growth event in the history of the ERCOT grid.