The Next Infrastructure Wave?

North American colocation vacancy dropped to a record low of 2.6% by the end of 2024, signalling the extraordinary pace at which data center demand is outstripping supply. This sharp decline occurred despite approximately 6.5 % of new capacity being under construction, with 72% of that space already pre-leased. The absorption rate is outpacing the completion of new developments, underscoring how rapidly hyperscalers (large-scale cloud service providers that offer computing) and enterprise customers are securing digital infrastructure to support artificial intelligence workloads, cloud services, and the broader digital economy. Simultaneously, power consumption by U.S. data centers is accelerating at a staggering pace, and electricity use is expected to nearly triple from 126 TWh (terawatt-hours) in 2022 to around 390 TWh by 2030, representing approximately 7 to 8% of national electricity consumption.

The global rise in AI-related data center usage is even more dramatic and in 2024, nine of the ten largest U.S. utilities identified data centers as their primary source of customer growth, Umweltbundesamt offers a mid-range forecast: AI-related energy use could climb from 30–50 TWh in 2023 to 73 TWh by 2026, with more extreme models projecting 200–500 TWh by 2027–2028. By 2030, the International Energy Agency projects that data centers will consume around 945 TWh globally, driven largely by AI workloads. This surge has triggered growing concern among energy providers and is reshaping energy investment and infrastructure planning.

Digital infrastructure or just a trend?

Data centers are increasingly being recognized as essential infrastructure, not just technology trends. Like traditional assets such as highways or power plants, data centers are now treated as long-term investments by REITs and infrastructure funds due to their stable, high-load demand, especially from hyperscalers and AI workloads. Local governments in Iowa, Kansas, Michigan, West Virginia, Utah, and Oklahoma are offering tax breaks, land grants, and infrastructure incentives to attract data center developments, much as they have historically competed for factories and stadiums. Each facility requires massive energy inputs, high-capacity fibre connectivity, and often water systems for cooling, placing a strain on utilities and mirroring the scale and complexity of traditional infrastructure projects.

What distinguishes the current boom is the migration of data center development into previously untapped markets, not due to dwindling demand, but rather to constraints in available power and land. This expansion echoes the surge in renewables of the 2010s and even the 1950s interstate highway build-out, as new hubs emerge in places like West Texas, Louisiana, and Columbus, Ohio. Utilities are scrambling to support these power-hungry sites, sometimes requiring four-year timelines just to connect to the grid. As a result, some developers are turning to interim solutions, such as natural gas turbines, or even exploring off-grid models. With construction still high and demand outpacing supply, data centers have become both a modern economic engine and a transformative force in land use, energy policy, and urban development.

Ripple effects across sectors

The rapid expansion of data centers across North America is putting immense pressure on utilities and the broader energy infrastructure. Power grid upgrades are now critical, with some utilities, such as Dominion Energy, grappling with multi-gigawatt power requests that are straining timelines and causing delays in grid interconnection projects. The traditional pace of energy infrastructure development is no longer adequate to meet the demands of the data economy. In response, major utility companies, such as Southern Company and American Electric Power (AEP), have revised their capital expenditure plans upward. Southern, for example, has shifted its forecast to a 6% annual load growth, significantly higher than the historic 1–2% range, attributed primarily to data center demand. To mitigate financial risks and ensure the feasibility of the build-out, utilities such as Duke Energy are introducing new contractual mechanisms. These include “take-or-pay” agreements, which obligate customers to pay regardless of usage, and upfront infrastructure contributions from data center developers, marking a notable shift in the dynamics between utilities and developers.

The surge in data center demand is reshaping the construction and real estate space. Projects dedicated to hyperscaler and colocation facilities now represent an increasingly dominant share of the engineering and construction workload. A Jones Lang LaSalle (JLL) report shows that 4.4 GW of capacity were absorbed in 2024 alone—quadruple the pace observed just four years ago. This growth is fueling an urgent demand for skilled labor, specialized contractors, and advanced project management capabilities. Firms like Sterling Construction report sustained backlogs tied explicitly to “mission-critical” data infrastructure, highlighting both the scale and complexity of current development cycles. Meanwhile, real estate developers and general contractors are adapting to evolving requirements regarding power access, water usage, and cooling technologies, all of which are influencing site design, material choices, and construction timelines.

The explosive growth in data centers is also creating ripple effects across regional economies and land-use frameworks, particularly in secondary markets such as Iowa, Georgia, and Phoenix. These areas offer a combination of lower land acquisition costs and access to more affordable utility services, making them attractive alternatives to legacy tech hubs. In turn, local governments are scrambling to adapt policies, expedite permitting processes, and scale public services to accommodate a new wave of digital infrastructure investment. However, these benefits come with growing pains. Communities are increasingly vocal about environmental impacts, especially around water consumption for on-site cooling and broader grid-powered water use. These concerns are leading to intensified scrutiny of planning processes and resource allocation, challenging municipalities to strike a delicate balance between economic opportunity and environmental stewardship.

Sustainability and resilience pressures

- Power constraints: Interconnection queues are growing. For instance, Virginia, among others, has moratoriums on new centers pending grid expansion. These delays highlight the mounting strain on legacy infrastructure as the digital economy outpaces utility upgrades.

- Environmental concerns: High water use and emissions are under review; Berkeley Lab projects data center electricity could reach 12% of U.S. load by 2028, and water usage could quadruple. These trends are drawing increased regulatory and public scrutiny, particularly in drought-prone or energy-constrained regions.

- Tech shifts: Edge computing and improved PUE (Power Usage Effectiveness) may moderate future growth, though current momentum appears sustained. While innovation helps mitigate impacts, efficiency gains are not yet sufficient to offset the explosive scale of AI and cloud demand.

Source: Stonehelp research

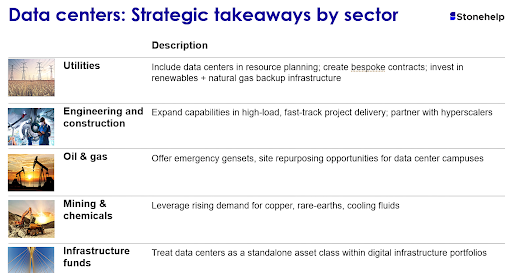

Strategic action for the days ahead

- Champion data centers as core infrastructure assets: Companies should align capital investments with land and energy availability while fostering utility partnerships. Early collaboration with utilities enables smoother grid extensions and reliable buffer capacity ahead of demand spikes

- Integrate energy efficiency and alternative cooling from the outset: Embed PUE/CUE targets in design and implement advanced cooling such as free-air economization, direct-to-chip, immersion cooling, or waterless systems where climate allows. These approaches lower energy and water consumption and promote resource resilience

- Engage regulators and communities proactively: Involve local decision-makers and residents early to build trust, transparently address environmental impact, and preempt delays; especially crucial in regions that face grid or freshwater constraints

- Expand strategically into emerging regions with flexible infrastructure models: Pursue locations offering incentives such as behind-the-meter power or microgrid districts and partner with utilities to co-develop adaptable grid ecosystems. This positions data centers not just as energy consumers but as contributors to resilient regional infrastructure