In Q1 2025, executives across the energy, utilities, chemicals and infrastructure sectors have been reacting to big changes in commodity prices, new government policies/tariffs, and global economic pressures. Brent crude averaged around $64 per barrel in Q1 2025 – a 20% drop from $80 per barrel in Q1 2024. This change has led many companies to rethink their strategies. Most are now focusing more on cutting costs, investing more carefully, and speeding up their shift toward cleaner energy. For example, natural gas prices in Europe have almost halved from $17/MMBtu in early 2024 to around $8.5/MMBtu in April 2025. This has affected profits for both upstream and downstream businesses. At the same time, refining margins have tightened in Asia and Europe, prompting chemical companies to adjust their portfolios and cut expenses. Still, despite these hurdles, some major energy companies have surprised investors with strong profits and cash flow, showing the impact of the changes they made over the past year. This mix of pressures and changes is shaping the outlook moving forward.

What’s been going on across key segments?

Upstream Energy

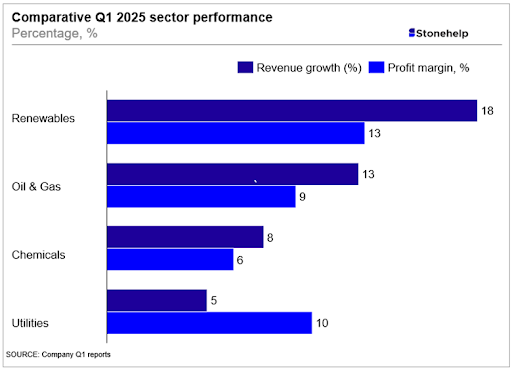

Upstream players are responding to a weaker oil price environment with a combination of capital discipline, operational efficiency, and shareholder returns. ExxonMobil exceeded expectations with $7.7 billion in profits, earnings of $1.76 per share, and $13 billion in cash flow. Its performance was driven by expansion in Guyana and the recently completed merger with Pioneer Natural Resources. These moves reinforce Exxon’s focus on scale in low-cost production zones. The question remains whether this scale advantage can insulate it from prolonged pricing pressure. Chevron reported $3.8 billion in adjusted profits, a 36% decline from Q1 2024. Yet it returned $3.9 billion to shareholders through dividends and buybacks, signaling continued confidence in its capital strategy. This raises questions about how Chevron is balancing short-term shareholder returns with long-term reinvestment, especially as market volatility continues. Shell reported $5.6 billion in adjusted profits, down 28% year-over-year, and announced a $3.5 billion share buyback. This capital return posture during a weaker earnings period suggests a conservative growth stance. Could this reflect a broader shift among European majors toward lower-risk capital allocation? BP’s performance was notably weaker, with profits declining nearly 50 percent to $1.4 billion due to trading losses and asset write-downs. TotalEnergies, in contrast, reported $4.2 billion in adjusted income, supported by strong trading performance and its LNG portfolio.

The divergence in results and strategic choices across companies highlights a broader industry question: are companies preparing for long-term structural change in oil markets, or positioning for cyclical rebound? The balance between cash preservation and growth investment will define who leads in the next phase of energy transition.

Downstream and Chemicals

The downstream and chemicals segment is contending with weak demand, especially from automotive and construction sectors. Dow Inc. experienced a 3% drop in net sales and has announced a target of $1 billion in cost reductions by 2026. These steps reflect expectations of continued market softness and margin compression. Feedstock cost increases and planned maintenance impacted earnings across the sector. Margin pressures were evident in olefins and polyurethanes, with limited pricing power. Phillips 66 reported a GAAP profit but posted an adjusted loss due to lower refining margins. These results highlight the tight operating conditions downstream players are facing. Companies are beginning to reassess capacity, with some initiating strategic adjustments in response to volatile input costs and sluggish end-market demand. There is increasing attention on portfolio optimization and regional dynamics, particularly in Asia, Europe, and North America. The path forward may require more fundamental changes in product mix and geographic footprint to protect profitability.

Utilities and Renewables

Utilities demonstrated resilience in the quarter, with NextEra Energy reporting a 9% increase in adjusted EPS. The gain was driven by the expansion of wind and solar projects, along with stable returns from regulated business lines. However, regulatory and policy uncertainty continues to present challenges. Debates over clean energy subsidies, permitting delays, and affordability concerns are gaining traction. In Illinois, rising electricity rates have prompted public policy discussions around grid reliability and cost management. In parallel, the sector is closely watching potential revisions to the Inflation Reduction Act and the EU Green Deal. These outcomes could directly influence investment planning and capital allocation. As utilities face competing pressures from regulators, investors, and consumers, the sector’s ability to maintain consistent returns while accelerating decarbonization will depend heavily on regulatory clarity and risk-sharing mechanisms. The need to proactively shape policy and manage expectations is becoming increasingly strategic.

Infrastructure and Industrial Players

The infrastructure sector remains cautiously optimistic, supported by strong backlogs in North America. Yet there are signs of strain. Delays in federal infrastructure funding, global supply chain disruptions, and inflationary cost pressures are weighing on execution. Companies are now evaluating the predictability of acquisitions versus the risks associated with new construction. Rising labor and material costs, alongside regulatory and environmental requirements, are altering the calculus for growth. These conditions are prompting a shift toward asset-light expansion and more selective project pipelines. There is also growing recognition that infrastructure investment cannot be viewed in isolation. Upstream cost control, downstream adjustments, and the overall investment climate are deeply interconnected. The need for greater strategic agility is clear. Successful players will be those that can navigate complexity, engage stakeholders effectively, and maintain delivery certainty in a high-cost, high-scrutiny environment.

Cross-cutting trends and strategic themes

A few clear patterns emerged from last quarter’s earnings calls.

The first is a clear emphasis on financial discipline. In the face of softening commodity prices and inflationary pressure, companies are taking a more measured approach to spending. Some are choosing to prioritise stable returns to shareholders through dividends and share buybacks (e.g., Shell), rather than making bold or risky investments. This signals a broader mindset shift towards caution, with executives closely watching every dollar.

Second is the growing importance of the energy transition. What once felt like a future ambition has now become a core part of most companies’ day-to-day strategies. From ExxonMobil’s work in carbon capture to TotalEnergies’ progress on clean fuels and Shell’s solar and wind expansions, these firms are no longer treating renewables as side projects. They are building them into the heart of their operating models. These efforts are being spurred by regulatory signals, changing customer preferences, and, increasingly, economic rationale as clean energy projects become more viable.

Third is digital transformations to enhance operational efficiency and resilience. Exxon is leveraging advanced digital technologies, including AI and machine learning, particularly in its Permian operations, to move towards closed-loop automation. Chevron is using AI-powered drones, the company remotely monitors its shale operations in Texas and Colorado, detecting issues such as emissions leaks and sending alerts to field teams. TotalEnergies continues to deploy AI for optimizing oil field production, predictive maintenance, and emissions reduction, while also supporting renewable energy development. These upgrades reflect a growing belief that innovation is not just a competitive edge, but it is now a survival tool.

Looking Ahead: What Leaders Should Prioritize for the Rest of 2025

As oil prices begin to stabilize but remain vulnerable to geopolitical shifts and OPEC+ decisions, companies are navigating a complex environment shaped by inflation, high interest rates, and uncertain demand. Across the value chain, upstream firms are focusing on low-cost, high-cash-flow projects. Utilities and renewables are awaiting policy signals to unlock long-term investment. Chemical producers are managing costs while monitoring demand recovery, and infrastructure players are aligning investments with public spending trends.

To stay ahead in this environment, leadership teams should prioritize the following:

- Strengthen operational resilience by advancing digital tools, automation, and predictive maintenance to reduce downtime and manage costs more effectively

- Reallocate capital to lower-risk, high-return investments that offer flexibility and preserve liquidity across changing conditions

- Engage actively with policymakers to shape regulatory outcomes and secure alignment on funding programs, especially in sectors reliant on public or policy-driven investment

- Institutionalize scenario planning to assess risks and opportunities across a range of market, policy, and technology outcomes.

The most effective leaders will not only adapt to uncertainty but actively shape their operating environment through smarter investments, strategic agility, and strong stakeholder engagement.